Victor Koech

September 23, 2024

If banks lived by their own advice, which is SAVE money, the banks would be loosing money. When you go and deposit 10,000 Kenyan shillings in the bank, that cash that you deposited is a liability for the bank.

An asset is something that puts money in your pocket. A liability is alternatively something that takes away money from your pocket.

So, when the bank has your cash, it’s a liability for them. Thus, they always want to get rid of it as fast as possible. And the way they do that is by lending it out because it’s an investment for the bank.

They don’t want to hold on to cash, but they want you to save your money. They want you to give them cash and just leave it there. But what is happening to your cash while it’s there?

It is losing value to inflation each and every day. Every day that you keep your cash in the bank, you’re becoming poorer each and every day.

In 2016, inflation was at 2 to 3% in the U.S. If you kept your cash in the bank, you have going broke every day till now when the inflation rate is at 8.5%. People may now thus now starting to realize that this inflation is a real problem.

When you keep your cash in the bank, the bank is paying 0.1%, maybe 0.5%, if you are lucky. They are then turning around lending for 5%, 6%.

So, the bank does not want to keep cash in savings because it’s a liability for them. The banks want you to keep spending money through card payments like debit and credit card because they will get to earn 18 to 25% in interest every time you spend one dollar of cash.

Even more sinister, governments want you to be financially uneducated. When you’re financially uneducated, guess what? You’re an employee and you’re a consumer. Who pays the highest taxes? Employees and consumers.

Everybody knows that rich people don’t pay taxes. It makes people angry, but a lot of times we don’t understand why. And we get angry at the wrong things and for the wrong reasons.

The more you make as a business owner, until you’re like uber rich, you will find that you’re spending a lot on taxes. But there are things you can do legally to pay less money in taxes. There also different ways that you can invest your money to pay less money in taxes.

There are a couple of examples. For instance, Tax Avoiding and Tax Evading are two similar words with two different outcomes.

Tax evading is illegal. You go to jail for it. On the other hand, tax avoiding is legal and then you get hated for doing it. But this is the way it works. You are playing within the rules of the system.

If you learn the revenue service code, it’s a rulebook. And the people who understand the rulebook are the people who have the money hire the good accountants and the good attorneys.

With an understanding of tax law, what happens is wealthy people will understand how this works, play within that system, and pay little to no money in taxes.

People netting millions in annual revenue can take various actions to avoid taxes better. This is assuming you have either some sort of your own income, you’re a side hustler, or you are a business owner. With 10 million in profit for instance, you are taxed on income. So, if you take out a salary that’s going to be taxed now, the question is what is a tax deduction? Or the better question is, how can you make something a tax deduction?

Anything can be a tax deduction, if you know how make it a deduction. So, that is the question you have to ask yourself because if you don’t have an income, you don’t have any tax.

The amount of tax a wealthy individual owes in a given year is an intricate web woven with waivers, deductions, credits, and hidden loopholes you've never heard of. Being debt free is the ideal. If you think it's not feasible, have a look at the 2021 analysis by nonprofit news site ProPublica of the tax filings of the wealthiest Americans that were obtained through leaks: Billionaires like Michael Bloomberg, Jeff Bezos, along with Elon Musk paid no taxes on federal income at all over a period of years.

So, do you wish to reduce your tax liability? Fantastic. Step 1: Become wealthy. Next, purchase a yacht, or perhaps a sports club. Donate generously to charity. Take a financial loss on the stock market. Above all, ensure that the majority of your money is held in assets rather than cash. Examples of assets include expensive jewelry, securities, real estate, paintings , and other items that catch your eye.

Spending lots of money to save a lot makes sense because when you're rich beyond belief, money doesn't really feel like an expense until a lot more zeros are added to the end. This explains why the extremely wealthy frequently employ pricey wealth managers, tax attorneys, or even open an entire office devoted to tax planning. There is a lot more work involved in planning, saving, offsetting, and attempting to minimize the taxes than just filing the return.

For wealthy individuals, filing taxes is a year-round undertaking rather than a simple springtime trip to the tax advisor.

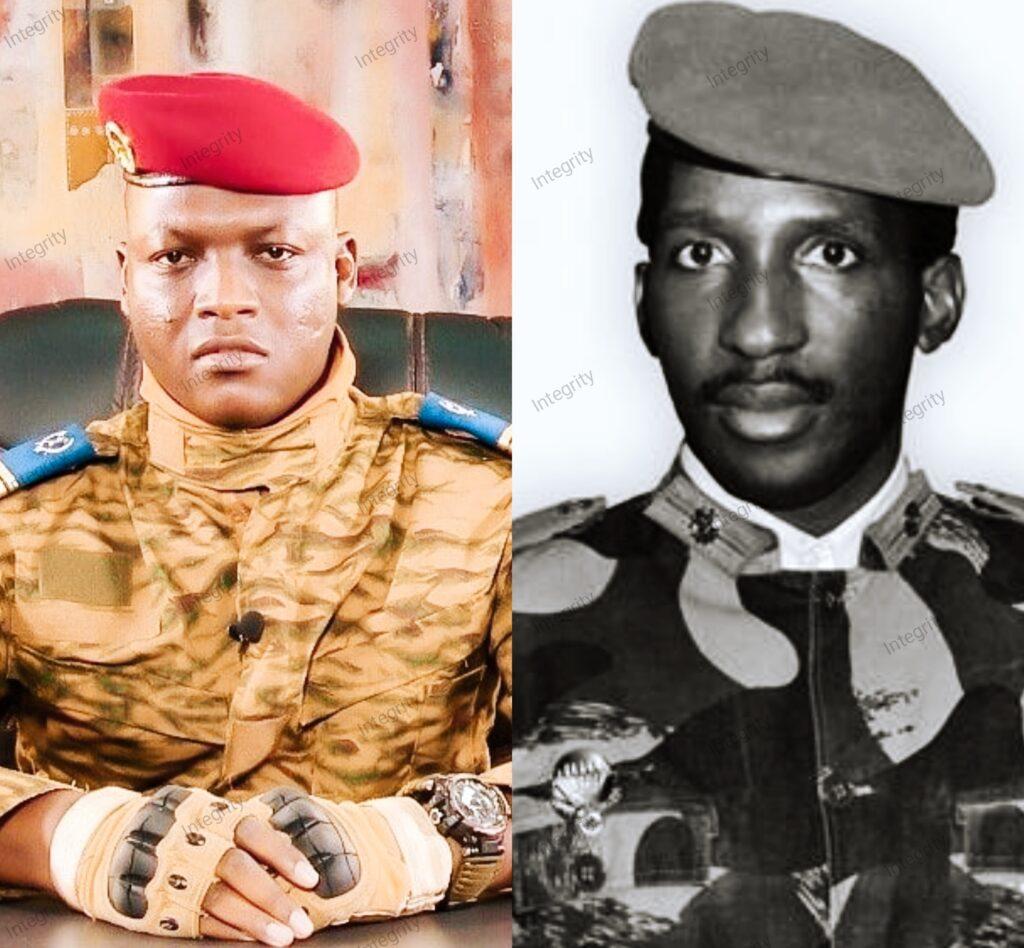

Ibrahim Traore, a Fulfilment of a Revolutionary’s Enduring Prophecy and the Emerging Face of True Pan-Africanism

1984: Is Kenya Descending into Orwell's Dystopian world?

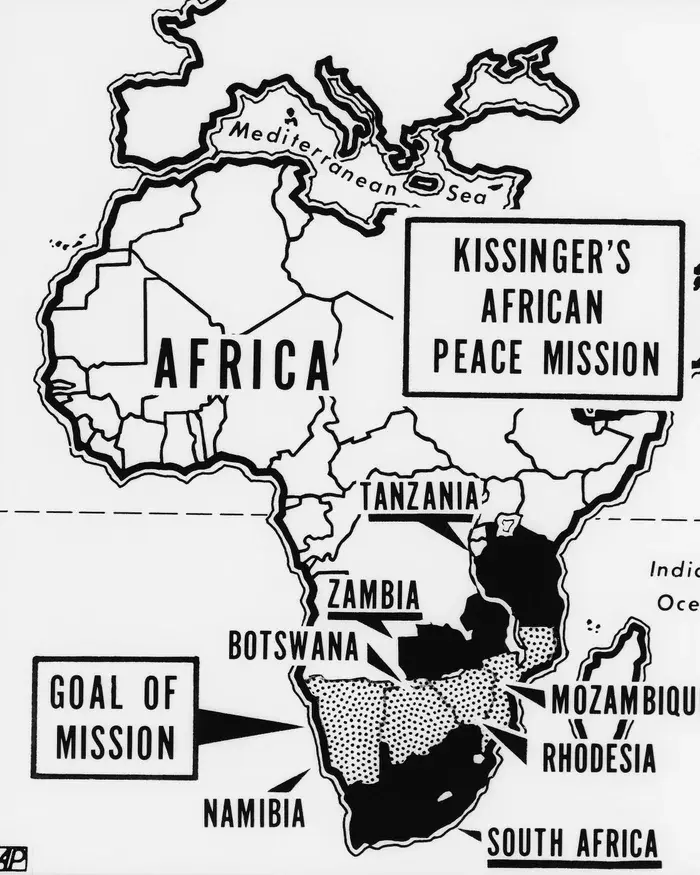

Kissinger Report, the Diabolical Policy Agenda to Depopulate Africa

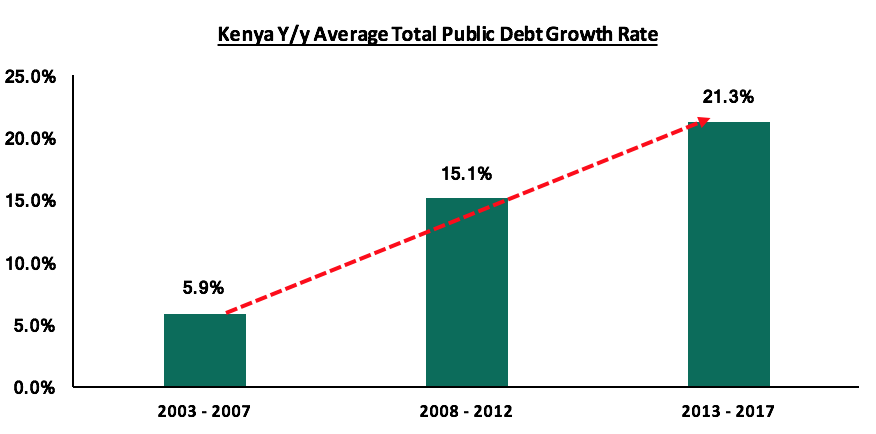

Increasing Domestic Borrowing Starves Kenyans Access to Private Business Loans

Push for a Cashless Society Threatens More Control, Taxation, and Surveillance of the Citizens

Money Lies That Keep You in Poverty