Victor Koech

July 10, 2024

A $2.75 billion sovereign bond was issued by Kenya to the international money markets less than one year after President Uhuru Kenyatta was elected in March 2013. This was completed in two parts. Together, the two offerings brought in $2.8 billion (Sh250 billion)—$2 billion in the first and $815 million (Sh74 billion) in the second. The government made an announcement about using the funds to reduce interest rates on official lending from its own market, which would encourage private investment.

According to economist David Ndii's findings, the government used the $2 billion loan to fund two transactions in an offshore account. It disbursed $604 million (Sh53 billion) to settle an outstanding debt and sent $394 million (Sh35 billion) to the national coffers, leaving $1.002 billion (Sh88 billion) in the account. This money has eluded the government's accounting efforts.

Government officials reacted with deceit and slurs when this was brought to their attention. In order to settle outstanding invoices with road contractors and provide financial assistance, the government made the false assertion that it had spent up to Sh120 billion. Still, Ndii stresses that the 2014–2015 fiscal year's recurrent budget was paid for by domestic resources; specifically, the government collected Sh1.106 trillion in taxes and sent Sh229 billion to the counties. This freed up Sh877 billion for use by the federal government. For that year, the national government's recurrent budget was Sh897 billion, which was just Sh20 billion higher than the income, clearly not reflecting the actual inflow of Sh120 billion. The national government could not have utilized the Sh88 billion given by the bond since their income shortfall was just Sh20 billion.

The Treasury pledged to disclose details on the initiatives supported by the Eurobond funds in its initial public announcement on the subject. The next week, it gave the ministries three weeks to provide the requested data. In a Business Daily interview conducted five weeks later, the Cabinet Secretary for Finance bemoaned the inability of the ministries to distinguish between funds obtained from the Exchequer that originated from domestic borrowing, VAT, income taxes, customs charges, excise taxes, and Eurobond payments. True, but it has nothing to do with the matter at hand. It was expected that Treasury would have the answer. The duty of monitoring and assessment falls on the government, as pointed out by Ndii. He harshly criticized the Treasury for what he called "downright irresponsible" spending tracking practices while disbursing the largest foreign loan ever.

The administration would "torture" the numbers in the months that followed to prove that development projects had been funded by the missing Eurobond funds. Nine projects in the energy industry had their budgets "wildly" inflated by Ndii, leading to roughly Sh67 billion in overruns. Electrifying elementary schools in remote regions reportedly cost Sh34 billion more than originally planned. An additional Sh62.8 billion was devoured by military modernization, an unallocated expense for the fiscal year. Ndii deduced that manipulating the numbers was done to fabricate a convincing narrative to account for the misplaced Eurobond funds. "How far does this deceit extend?" he inquired.

The government was unable or unable to provide a straight response to this issue; but, its actions in the subsequent years reeked of adultery caught red-handed. David Ndii claims that the government's inability to reconcile its books while spending the Eurobond funds that it hadn't used was the true issue. By lowering domestic borrowing from Sh251 billion to Sh110 billion for the 2014–15 fiscal year, it managed to accomplish this feat to some extent. Its purported carryover of Eurobond funds from 2013–14 was fully offset by the Sh140 billion cut. Regrettably, this magical accounting was ruined by the Central Bank's domestic borrowing accounts, and the interest that the government claimed to have paid on domestic borrowing that year was completely at odds with it.

By doing a forensic audit of Eurobond transactions from the Federal Reserve Bank of New York in 2016, Auditor General Edward Ouko sought to uncover the truth. He informed lawmakers that he had already scheduled meetings with prominent US and UK financial firms participating in the deals as part of his preparations. Among the financial institutions that were involved in the $2 billion Eurobond transactions were JP Morgan, the Federal Reserve Bank, City Transaction Services New York, JP Securities, Barclays Bank, ICB Standard Bank, Qatar National Bank, and others; Mr. Ouko had pledged to dispatch forensic auditors to probe these institutions.

The inquiry was immediately stopped by Mr. Kenyatta, who fancifully claimed that Mr. Ouko's claim that "the Eurobond money had been stolen and stashed within the Federal Reserve Bank of New York" showed collusion between the US government and the Kenyan government. The president remarked with a hint of disdain, "Who is stupid here?"

Over the following years, the administration grew increasingly arrogant and aggressive. Since the Auditor General has been unable to follow the worldwide trail of money, he or she has been content to inform Parliament at the end of each audit year that investigations into the handling, accounting, and utilization of funds pertaining to the sovereign/Eurobond are continuing and that the veracity of the net proceeds of Kshs 215,469,626,035.75 has not been determined.

Finding a solution to this mystery shouldn't have been as difficult as the Auditor General's brief conclusion made it out to be, according to Ndii's study. The Treasury's attempts to clarify the situation, aided by the International Monetary Fund, made matters worse. The IMF, however, has acted with criminal negligence in these regards, as the Mozambique Eurobond scandal demonstrates.

Attempts by the IMF to assist the government in this instance were unsuccessful. Eurobond funds were received and used throughout the 2013–14 fiscal year, as the Fund verified. It was not possible to spend the Eurobond money that the Fund received in the last week of that fiscal year because of other commitments. Prior to the beginning of the 2014–2015 fiscal year in the inaugural week of July, no withdrawals were made. While the Treasury recorded a domestic borrowing number of Sh110 billion for 2014/15, the IMF reported a total of Sh251 billion, highlighting the discrepancy in the two entities' manipulations. According to Ndii, the Treasury does the exact opposite of what the IMF does with its records.

The misrepresentation by the Treasury was made worse by the Mandarins' forgetfulness. They appeared to have completely disregarded the 2014/2015 figures by 2015/2016. The official sum for domestic borrowing has now been released by the Treasury at Sh251 billion. Identifying the projects that received the Sh140 billion Eurobond funding was the only way to explain it once the Treasury certified the right amount of Sh251 billion. Without specific projects to point to, it's safe to assume that the $1 billion in Eurobond money have disappeared. I think it's safe to say that some senior untouchables have taken it.

With no investigations, the President intimidating the Auditor General, and the United States (especially the New York Federal Reserve) showing a conspicuous lack of enthusiasm, it is unlikely that we will find out who stole over $1 billion in taxpayer money.

Ibrahim Traore, a Fulfilment of a Revolutionary’s Enduring Prophecy and the Emerging Face of True Pan-Africanism

1984: Is Kenya Descending into Orwell's Dystopian world?

Kissinger Report, the Diabolical Policy Agenda to Depopulate Africa

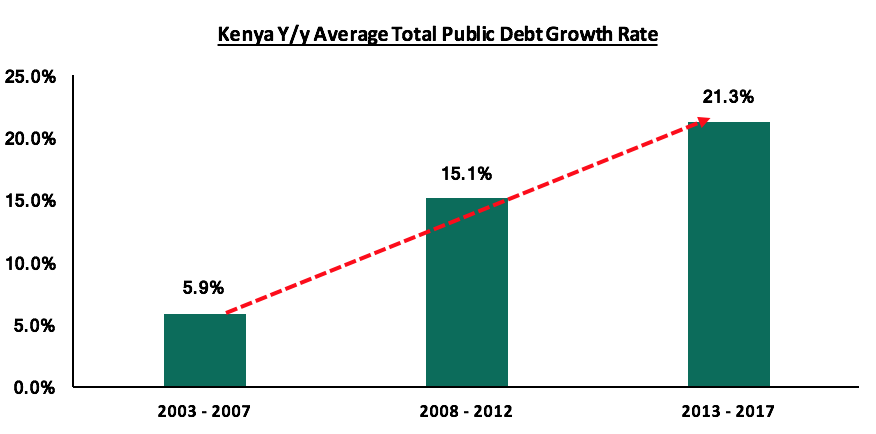

Increasing Domestic Borrowing Starves Kenyans Access to Private Business Loans

Push for a Cashless Society Threatens More Control, Taxation, and Surveillance of the Citizens

Money Lies That Keep You in Poverty