Victor Koech

September 6, 2024

We are witnessing a shift in labour patterns as the elder members of Generation Z join the workforce. While they may not be contemplating financial investments since they do not have any big financial obligations, they should be considering wealth growth or asset protection.

Given their low levels of discretionary income, however, this demographic would do well to prioritise wealth preservation over wealth creation, as the latter only leads to further accumulation of wealth.

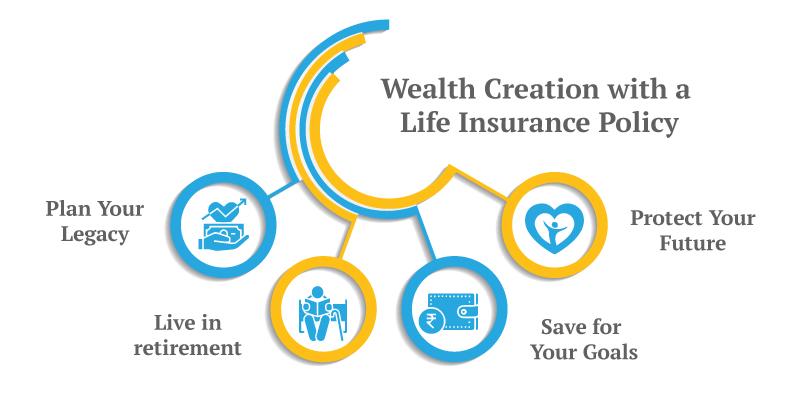

While investing allows us a limitless array of options including stocks, treasury bills, bonds, money market funds, and more, protecting our loved ones from financial losses is the primary goal of asset preservation. Life insurance has a role in this context.

In life insurance, the policyholder agrees to pay premiums to the insurance company on a regular basis, and the insurer agrees to pay out a benefit to the policyholder's designated dependents upon the policyholder's death.

Those members of Generation Z who aren't yet comfortable with leaving a large financial legacy will find this especially important. The individual's dependents might utilise the death benefit to pay for their expenditures.

Kenya offers three types of life insurance: term life, full life, and endowment insurance. The most basic and affordable type of insurance is term life insurance.

It provides coverage for a specific period of time, typically ten, twenty, or thirty years. Whole life insurance covers a person's whole life and accumulates monetary value over time.

Endowment insurance combines elements of both term life and savings policies; it pays out either to the policyholder or their dependents in the event of the policyholder's death or the policy's term ends.

As a result, life insurance can be bought from a number of sources such as insurance companies and banks. Different insurers provide essentially the same plans; what sets them apart is mostly the quality and desirability of their features.

Endowment policies begin at Sh1,000 monthly and final expense insurance at Sh900 annually.

What is the point of having life insurance?

Kenya is home to more than 50 million people, although the country's industry penetration rate stands at a dismal 1.3%. Now is a good time to invest. In addition, there are several benefits to acquiring a life insurance policy.

One major benefit of life insurance is the peace of mind it gives to loved ones in the unfortunate event of an unexpected death. Beneficiaries may get a lump sum payment to use for things like last expenses, debt repayment, and living costs.

Second, life insurance can help you save money. Take whole life insurance as an example. It lets you build cash worth that you can use for retirement or future expenses.

Furthermore, with an endowment, you can set aside a portion of your death benefit to go towards a particular purpose, like launching a business.

Finally, in Kenya, life insurance gives tax benefits. You can get more money out of your life insurance policy because premiums are tax deductible and the death payout is usually tax free.

It is critical to understand the expenses associated with life insurance.

Premiums are determined by factors like as age, health status, and coverage amount. Other policy components, like as exclusions, limits, and riders, are crucial. For example, certain insurance policies may exclude coverage for fatalities caused by specific activities or circumstances.

The aforementioned considerations should guide millennials and Generation Z while shopping for life insurance in Kenya.

Ibrahim Traore, a Fulfilment of a Revolutionary’s Enduring Prophecy and the Emerging Face of True Pan-Africanism

1984: Is Kenya Descending into Orwell's Dystopian world?

Kissinger Report, the Diabolical Policy Agenda to Depopulate Africa

Increasing Domestic Borrowing Starves Kenyans Access to Private Business Loans

Push for a Cashless Society Threatens More Control, Taxation, and Surveillance of the Citizens

Money Lies That Keep You in Poverty